FHA, VA, USDA, and conventional mortgages for HUD-code manufactured homes. Finance your home and land together with as little as 0% down.

Your home must meet these standards to qualify for mortgage financing.

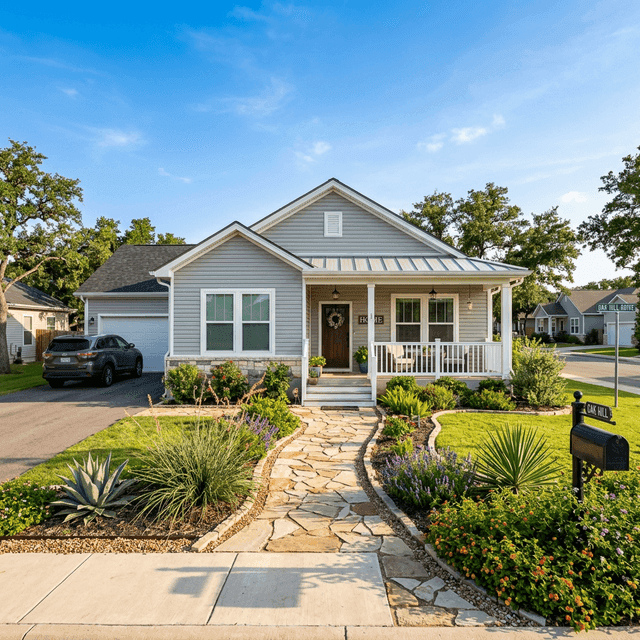

Your manufactured home must be built after June 15, 1976 and display a HUD certification label. Pre-1976 'mobile homes' are not eligible for most mortgage programs.

The home must be permanently affixed to a foundation that meets HUD or local code requirements. Wheels, axles, and hitches must be removed.

The manufactured home must be titled as real property (real estate), not personal property. Texas allows conversion from personal to real property through the county.

For FHA, VA, USDA, and conventional loans, you must own the land (or purchase it simultaneously). Leased-land homes require chattel financing.

FHA, VA, and USDA loans require the manufactured home to be your primary residence. Conventional loans may allow second homes in some cases.

Most mortgage programs require a minimum of a double-wide (multi-section) manufactured home. Some FHA programs accept single-wide with restrictions.

Manufactured homes deliver modern quality at 30–50% less than site-built — and qualify for the same mortgage programs. Compare scenarios in our mortgage calculator.

Combine the manufactured home purchase and land into a single mortgage. No separate land loan needed. Your loan covers the home, land, transportation, and installation.

Manufactured homes cost $55–$130 per square foot vs. $150–$250 for site-built. A 2,000 sq ft manufactured home can save you $100K–$200K compared to new construction.

FHA, VA, USDA, and conventional loans for manufactured homes follow the same guidelines and offer similar rates as site-built home mortgages.

Already own the land? Your land equity can serve as your down payment, potentially eliminating the need for cash out of pocket.

FHA vs. VA vs. Conventional vs. Chattel — side by side.

Understanding the difference — and why real property wins.

From pre-approval to move-in.

We assess your credit, income, and land situation to identify the best program — FHA, VA, USDA, or conventional. Pre-approval typically takes 24–48 hours.

Choose your manufactured home from a dealer or private seller. If you don't own land, we finance the land purchase simultaneously in one loan.

Your home is installed on a permanent foundation. We coordinate the real property conversion with your county so the home is titled as real estate.

One closing covers everything: home, land, foundation, and installation. Your loan converts to a standard 30-year mortgage. Welcome home.

Common questions about financing manufactured and mobile homes in Texas.

FHA • VA • USDA • Conventional — all available for manufactured homes.

Check my eligibility